FHA vs. conventional loan, choosing the right mortgage can be a daunting task. This guide will help you understand the key differences between FHA and conventional loans, exploring their advantages, disadvantages, and suitability for various financial situations.

We’ll delve into eligibility criteria, interest rates, down payment requirements, and the loan application process for both types. This comprehensive comparison will empower you to make an informed decision about which loan option best aligns with your financial goals and homeownership aspirations.

Introduction to Loan Types

Understanding the nuances of different loan types is crucial for making informed financial decisions. This section delves into the specifics of FHA and conventional loans, outlining their key characteristics, eligibility requirements, and associated costs. Knowing the differences will help you determine which loan best suits your individual financial circumstances.

FHA Loans

FHA loans, or Federal Housing Administration loans, are government-backed mortgages. This backing reduces risk for lenders, making them more accessible to borrowers with less-than-perfect credit or a smaller down payment. FHA loans often come with more lenient eligibility requirements than conventional loans.

Conventional Loans

Conventional loans are mortgages not insured by the government. These loans are typically offered by private lenders and often require a larger down payment and better credit history than FHA loans. Lenders assess borrowers’ creditworthiness and financial stability more stringently.

Eligibility Criteria

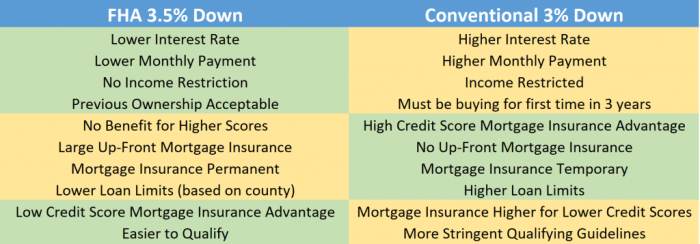

FHA loans generally have less stringent eligibility requirements compared to conventional loans. These requirements can include lower credit scores and smaller down payments. Conventional loans, conversely, necessitate a stronger credit history and a larger down payment, which can vary depending on the lender and loan type.

Comparison Table

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Interest Rate | Potentially slightly higher than conventional loans due to government backing, but can vary widely. | Typically lower than FHA loans, as they are not backed by the government, although it can vary. |

| Down Payment | As low as 3.5% is possible, with a higher amount potentially needed depending on specific circumstances. | Usually requires a down payment of 5% or more, but can vary with different loan programs. |

| Closing Costs | Potentially higher than conventional loans due to government involvement. | Typically lower than FHA loans due to the absence of government involvement, but can vary based on loan terms. |

| Credit Score | Generally lower credit scores are acceptable. | Usually requires a higher credit score. |

The table above provides a general comparison, but the specific interest rates, down payments, and closing costs will vary significantly based on individual circumstances, including the lender, the current economic climate, and loan terms.

FHA Loan Advantages

FHA loans, backed by the Federal Housing Administration, offer attractive features for homebuyers. They often provide a pathway to homeownership for individuals who may not meet the stringent criteria of conventional loans. Understanding the benefits of FHA loans can help potential homeowners make informed decisions.FHA loans are particularly advantageous due to their accessibility. They are designed to assist a wider range of borrowers, often those with smaller down payments or less-than-perfect credit scores, in achieving their dream of homeownership.

This accessibility makes FHA loans a popular choice for many first-time homebuyers and those in specific financial situations.

Down Payment Requirements

FHA loans typically require a lower down payment than conventional loans. This is a significant advantage, particularly for first-time homebuyers or those with limited savings. The minimum down payment for an FHA loan is typically 3.5%, significantly lower than the 20% often required for conventional loans. This reduced down payment requirement allows buyers to access homeownership with a smaller upfront investment.

This reduced barrier to entry makes homeownership more achievable for a wider range of individuals.

Credit Score Requirements

While a strong credit score is always beneficial for any loan, FHA loans often have more lenient credit score requirements than conventional loans. This makes homeownership accessible to individuals with slightly less-than-ideal credit histories. While a minimum credit score is still required, it often allows for a smoother application process compared to more stringent requirements.

Eligibility Considerations

FHA loans are often a suitable choice for first-time homebuyers, those with limited savings, and those with slightly less-than-ideal credit scores. Furthermore, FHA loans can be a good option for individuals who need to navigate a challenging financial situation to reach homeownership. For example, a recent graduate who has just started their career or a family who is rebuilding their finances after a hardship might find FHA loans more accommodating.

Pros and Cons of an FHA Loan

| Pros | Cons |

|---|---|

| Lower down payment requirements (3.5% minimum) | Higher closing costs compared to conventional loans |

| More accessible to borrowers with lower credit scores | Potentially higher interest rates compared to conventional loans in certain situations |

| Government backing, leading to more favorable terms for the borrower | Stricter underwriting guidelines |

| Can be suitable for a wider range of buyers | Limited loan amounts for some areas |

Conventional Loan Advantages

Conventional loans offer a wide range of benefits for homebuyers, often presenting a more straightforward and potentially more favorable financing option compared to FHA loans. These loans are typically available to a broader range of borrowers, reflecting a greater reliance on the borrower’s creditworthiness and financial capacity.Conventional loans frequently provide more flexibility in terms of down payment requirements, potentially allowing for lower monthly payments.

This aspect is particularly appealing to buyers with limited financial resources.

Credit Score Requirements

Conventional loans generally have higher credit score requirements compared to FHA loans. Lenders assess creditworthiness to evaluate the risk associated with the loan. A higher credit score demonstrates a stronger repayment capacity, thereby reducing the risk for the lender. A strong credit history, typically involving timely payments and a low debt-to-income ratio, is essential to qualify for a conventional loan with favorable terms.

This can be a significant advantage for borrowers with excellent credit.

Down Payment Requirements

Conventional loans often allow for lower down payments than some other types of loans. This characteristic can be advantageous for homebuyers with limited funds. The minimum down payment for a conventional loan can vary depending on the specific loan program and the appraised value of the property. However, a down payment as low as 5% is possible for certain conventional loans, allowing homebuyers with limited savings to enter the housing market.

Many borrowers utilize their savings or take out a separate loan for the down payment.

Examples of When a Conventional Loan is a Better Option

Conventional loans are frequently a better option for borrowers with excellent credit histories and substantial savings, who may be seeking a lower interest rate or greater flexibility in loan terms. Borrowers with strong credit and high incomes are more likely to qualify for more favorable loan terms and lower interest rates with conventional loans. For example, a buyer with a 750+ credit score and substantial savings may find a conventional loan a more appealing option than an FHA loan, given the potential for a lower interest rate and fewer loan restrictions.

Additionally, buyers who wish to put a larger down payment or do not need the government guarantee may find a conventional loan preferable.

Conventional Loan Pros and Cons, FHA vs. conventional loan

| Feature | Pros | Cons |

|---|---|---|

| Credit Score Requirements | Generally higher credit score requirements can lead to more favorable terms and lower interest rates for those with excellent credit. | Higher credit score requirements may exclude some borrowers. |

| Down Payment | Potentially lower down payments are available for certain programs compared to other loans. | A larger down payment may be necessary in some situations. |

| Interest Rates | Conventional loans often have lower interest rates for those with strong credit. | Interest rates can fluctuate based on market conditions. |

| Loan Terms | Conventional loans may offer more flexibility in loan terms, potentially allowing for more customized solutions. | More stringent requirements may exist for specific loan programs, limiting options. |

| Loan Restrictions | Fewer restrictions compared to FHA loans may lead to more options. | Potential for stricter lending standards in specific economic climates. |

Loan Application Process

Navigating the loan application process can feel daunting, but understanding the steps involved for both FHA and conventional loans can significantly ease the process. Thorough preparation and a clear understanding of the requirements for each loan type are key to a smooth application.The application process for both FHA and conventional loans involves a series of steps and documentation requirements.

The timeframes can vary depending on factors such as lender processing speed and the applicant’s completeness in providing all necessary information. It’s crucial to be prepared and organized throughout the process.

FHA Loan Application Process

The FHA loan application process typically begins with pre-qualification, where borrowers estimate their loan eligibility based on their financial situation. This step helps borrowers understand the amount they can borrow and assists in setting realistic expectations. This step helps borrowers avoid unnecessary complications later in the process. The next step involves submitting a formal loan application, which often includes completing a comprehensive application form and gathering supporting documentation.

Detailed information about income, assets, and debts are needed.

Conventional Loan Application Process

Similar to FHA loans, the conventional loan application process begins with pre-qualification. This preliminary step determines the loan amount a borrower might be eligible for. This crucial step helps avoid potential problems later on in the process. Following pre-qualification, the application is submitted, often requiring comprehensive financial information and supporting documents. This process includes providing details about income, assets, debts, and credit history.

Required Documents and Procedures

Both FHA and conventional loans demand specific documentation. Common documents include pay stubs, tax returns, bank statements, and proof of employment. The specific requirements may vary based on the lender. The lender will usually provide a detailed list of required documents to streamline the process.

Timeline

The timeline for loan applications can vary. Factors like the completeness of the application and lender processing times influence the duration. Generally, the process can take anywhere from several weeks to a few months. For example, a borrower who provides all required documents promptly may see a quicker processing time than one who is slow in providing the required documents.

Some lenders offer online portals or other convenient tools to track the application’s progress.

Comparison Table: FHA vs. Conventional Loan Application

| Step | FHA Loan | Conventional Loan |

|---|---|---|

| Pre-qualification | Estimate loan eligibility based on financial situation. | Estimate loan eligibility based on financial situation. |

| Application Submission | Complete application form, provide supporting documentation. | Complete application form, provide supporting documentation. |

| Documentation Requirements | Income, assets, debts, credit report, proof of residency. | Income, assets, debts, credit report, proof of residency. |

| Processing Time | Generally 4-6 weeks, but can vary. | Generally 4-6 weeks, but can vary. |

| Approval/Disapproval | Based on FHA guidelines and lender criteria. | Based on lender criteria and loan terms. |

Credit Score Requirements

A crucial factor in securing either an FHA or conventional loan is your credit score. Lenders use credit scores to assess your creditworthiness, determining your likelihood of repaying the loan. Understanding the different requirements and factors affecting these scores is essential for a successful loan application.Credit scores play a pivotal role in loan approvals, as they indicate your repayment history and financial responsibility.

Higher credit scores generally translate to lower interest rates and better loan terms, making it more financially advantageous to have a strong credit history. Lenders rely heavily on credit scores to manage risk, and applicants with weaker scores might face more stringent requirements or higher interest rates.

FHA Loan Credit Score Requirements

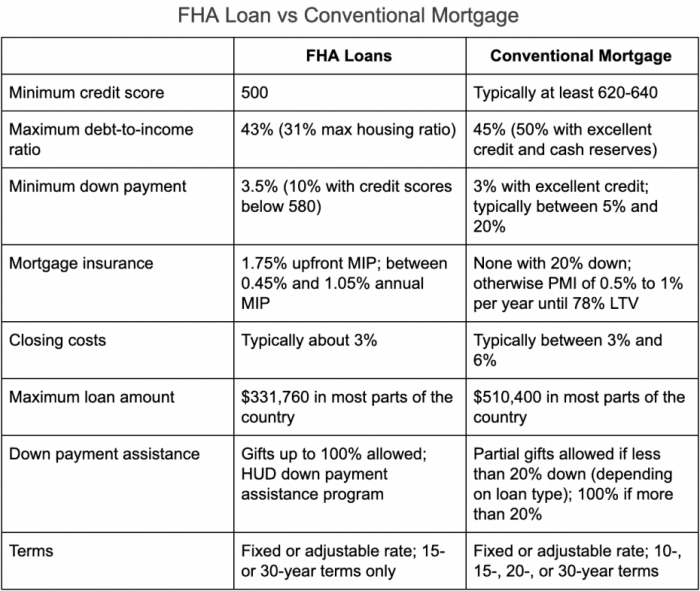

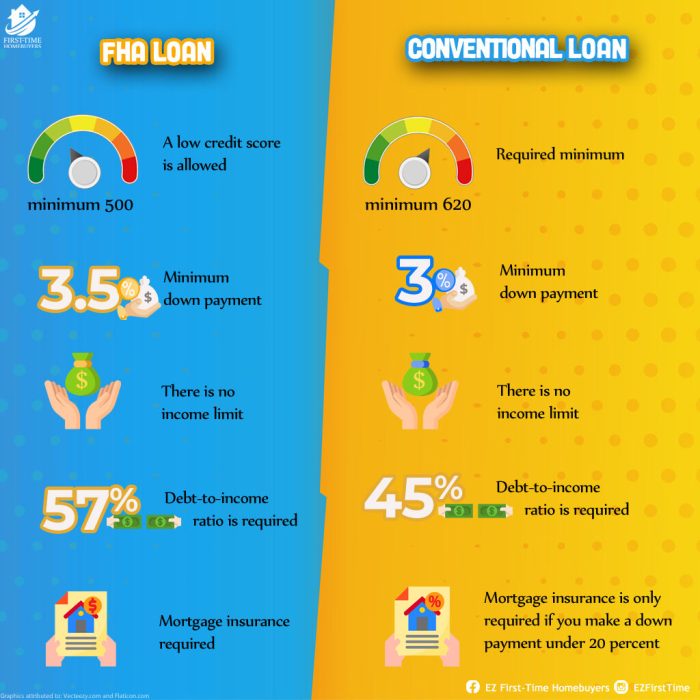

FHA loans, designed to assist homebuyers with lower credit scores, typically have more lenient credit score requirements compared to conventional loans. While there’s no specific minimum credit score, lenders often prefer scores above 580. However, borrowers with scores below 580 might still be eligible if they demonstrate strong financial stability through other means, such as a significant down payment or a co-signer.

Conventional Loan Credit Score Requirements

Conventional loans, on the other hand, often demand higher credit scores. A score of 620 or above is frequently the threshold for approval, though this can vary based on individual circumstances. Lenders meticulously evaluate the borrower’s credit history to determine their risk profile.

Factors Affecting Credit Score Requirements

Several factors influence the specific credit score requirements for both loan types. These factors include:

- Loan Amount: Larger loan amounts often require higher credit scores to demonstrate the borrower’s ability to repay the debt.

- Down Payment: A larger down payment can mitigate risk for the lender, potentially allowing for lower credit score requirements.

- Debt-to-Income Ratio (DTI): A lower DTI, reflecting a manageable level of debt compared to income, usually increases the chances of loan approval, regardless of the credit score.

- Loan Type: Specific types of conventional loans might have different credit score criteria. For instance, a loan with a smaller down payment may require a higher credit score.

- Overall Financial Stability: Lenders consider the borrower’s overall financial picture, including employment history, income stability, and savings. A consistent and substantial income demonstrates greater reliability.

Importance of Credit Score in Loan Approvals

A strong credit score significantly impacts the loan approval process. It directly affects the interest rate offered, the loan terms, and the potential for approval. A higher credit score often results in lower interest rates, which translates to substantial savings over the life of the loan.

Credit Score Range and Eligibility Comparison

| Loan Type | Credit Score Range (Approximate) | Eligibility |

|---|---|---|

| FHA Loan | 580 or higher, but may consider factors like down payment and DTI. | Generally more lenient than conventional loans, especially for those with lower scores. |

| Conventional Loan | 620 or higher, with potential variations based on specific circumstances. | Typically requires a higher credit score to demonstrate greater financial stability. |

Down Payment Requirements

A crucial factor in homeownership is the down payment. The amount you put down upfront significantly impacts your monthly payments and overall affordability. Understanding the differences in down payment requirements for various loan types is essential for making informed decisions.

FHA Loan Down Payment Requirements

The Federal Housing Administration (FHA) insures loans, allowing for lower down payments than conventional loans. This is a key advantage for buyers with limited savings. FHA loans typically require a down payment of 3.5% of the home’s purchase price. However, this minimum down payment can vary based on the specific loan program. For example, a higher down payment might qualify the borrower for better interest rates or potentially other favorable loan terms.

Conventional Loan Down Payment Requirements

Conventional loans, unlike FHA loans, don’t require government backing. This often translates to a higher required down payment. The minimum down payment for a conventional loan can vary widely, often ranging from 5% to 20% of the home’s purchase price. A higher down payment can lead to a lower interest rate, potentially saving you money in the long run.

There are also various conventional loan types, including those that allow for lower down payments (such as FHA loans). Many lenders offer different programs with varying down payment requirements to suit the buyer’s financial situation.

Impact on Affordability

Down payment requirements significantly affect affordability. A lower down payment, as offered by FHA loans, reduces the initial cash outlay, potentially making homeownership more accessible to a wider range of buyers. Conversely, higher down payments associated with conventional loans might make homeownership less attainable for some. For instance, a buyer with a limited budget might find an FHA loan more manageable than a conventional loan with a substantial down payment requirement.

Comparison Table

| Loan Type | Typical Down Payment (%) | Potential Impact on Affordability |

|---|---|---|

| FHA Loan | 3.5%

| Potentially more accessible, reducing the upfront cash needed for a home purchase. |

| Conventional Loan | 5%

| Potentially less accessible, requiring a larger initial investment. |

Pre-Approval Process

The pre-approval process is a crucial step for homebuyers, providing a clear understanding of their borrowing capacity and strengthening their negotiating position. This process allows potential homebuyers to know precisely how much they can afford to borrow, which helps them focus their search on properties within their financial means. A pre-approval letter, backed by a formal assessment, significantly boosts a buyer’s credibility in the eyes of sellers.

Understanding the Pre-Approval Process

The pre-approval process evaluates a buyer’s financial readiness to secure a loan. This assessment involves a review of their creditworthiness, income, debts, and assets to determine the maximum loan amount they qualify for. This pre-approval process is tailored to the specific loan type, considering the unique requirements of FHA and conventional loans.

Benefits of Pre-Approval for Homebuyers

A pre-approval letter offers several advantages for homebuyers. It sets clear financial boundaries, preventing overspending on a home. This letter serves as a powerful tool when making offers, demonstrating financial commitment and seriousness. It can also help negotiate more favorable terms with sellers. Furthermore, it fosters confidence in the homebuying process.

Steps Involved in Obtaining Pre-Approval

The steps involved in pre-approval are generally similar for both FHA and conventional loans. First, the buyer contacts a lender to initiate the process. Next, the lender gathers necessary financial documents, verifies information, and assesses the buyer’s creditworthiness. Finally, the lender issues a pre-approval letter detailing the maximum loan amount the buyer qualifies for. The duration of this process varies depending on the lender and the completeness of the submitted documentation.

Choosing between an FHA and a conventional loan is a key decision when navigating the home-buying process. Understanding the nuances of each loan type is crucial for successful homeownership, particularly when considering the various aspects of Buying & Selling Homes. Ultimately, the best choice depends on individual financial situations and goals, but understanding these loan options will help buyers make the right decision for their circumstances.

Documents Required for Pre-Approval

The precise documentation required for pre-approval varies based on the lender’s policies and specific loan types. However, common documents for both FHA and conventional loans include:

| Document Category | Typical Documents |

|---|---|

| Personal Information | Social Security Number, Driver’s License, Proof of Residency |

| Income Verification | Pay stubs, tax returns, W-2 forms, or other relevant income documentation |

| Debt Information | Bank statements, credit card statements, loan documents, and any other debt obligations |

| Asset Information | Bank statements, investment records, and other asset documentation |

This table presents a concise overview of the documents frequently required for pre-approval. The specific documents needed might differ based on the lender and the loan type. It’s essential to contact a lender directly to confirm the complete list of required documents. The lender will provide a detailed list of specific documentation based on the chosen loan type.

Choosing the Right Loan: FHA Vs. Conventional Loan

Deciding between an FHA and a conventional loan involves careful consideration of individual financial circumstances and the unique characteristics of each loan type. A thorough understanding of these factors can significantly impact the long-term financial health of a homebuyer. Weighing the advantages and disadvantages of each option is crucial to making an informed decision.

Factors Influencing Loan Choice

Understanding individual financial situations is critical in selecting the appropriate loan. Income stability, credit score, and the desired down payment amount significantly influence the loan type that best suits an individual’s needs. For instance, a buyer with a high credit score and substantial savings might be better positioned for a conventional loan, which often offers more favorable terms.

Conversely, a buyer with a lower credit score might find an FHA loan a more accessible option.

Choosing between an FHA and a conventional loan depends on various factors, like your credit score and down payment. Ultimately, the best approach might involve exploring options like a best cryptocurrency wallet for alternative investment strategies, which could influence your financial situation and potentially impact your loan approval. This is just one of many factors that might impact your decision regarding FHA vs.

conventional loans.

Comparison of Loan Types

A detailed comparison of FHA and conventional loans reveals key differences in their terms and conditions. These differences directly impact the loan application process and the overall cost of homeownership.

- Down Payment Requirements: FHA loans typically require a smaller down payment (3.5%) compared to conventional loans (often 5% or more). This lower down payment requirement can make FHA loans more accessible to buyers with limited savings. However, this accessibility comes with additional costs, such as mortgage insurance premiums.

- Credit Score Requirements: FHA loans have slightly less stringent credit score requirements than conventional loans. While a good credit score is always beneficial, an FHA loan might be a viable option for buyers with a credit score below the threshold for a conventional loan. However, a lower credit score might mean higher interest rates.

- Mortgage Insurance Premiums (MIP): A crucial difference is mortgage insurance. FHA loans require mortgage insurance premiums (MIP), which are ongoing payments throughout the life of the loan, while conventional loans often do not. While MIPs add to the overall cost of the loan, they can potentially make homeownership more attainable for buyers with lower down payments.

- Interest Rates: The interest rates for both loan types are influenced by various factors like the borrower’s creditworthiness, market conditions, and the specific lender. While the rates may vary, generally, conventional loans can offer slightly lower interest rates than FHA loans, particularly for borrowers with excellent credit.

Summary Table

| Factor | FHA Loan | Conventional Loan |

|---|---|---|

| Down Payment | 3.5% (or less) | 5% or more |

| Credit Score | Lower acceptable scores | Higher acceptable scores |

| Mortgage Insurance | Required (MIP) | Typically not required |

| Interest Rates | Potentially higher | Potentially lower |

| Accessibility | More accessible for buyers with limited savings | More favorable for buyers with substantial savings and strong credit |

Conclusive Thoughts

Ultimately, the decision between an FHA and conventional loan hinges on your unique financial circumstances. Weighing the pros and cons of each, considering your credit score, down payment capabilities, and desired loan terms, will lead you to the most suitable option for achieving your homeownership dreams. This comparison highlights the crucial factors to consider, equipping you with the knowledge needed for a successful home buying journey.

FAQs

What are the typical closing costs for each loan type?

Closing costs vary significantly depending on the location and specific loan terms. However, FHA loans often have slightly higher closing costs compared to conventional loans due to the government-backed insurance premium. Always consult with a lender for personalized cost estimates.

How long does the loan application process typically take?

The timeframe for loan application processing can fluctuate based on various factors, including lender workload, required documentation, and the complexity of the application. A general guideline would be to anticipate a 30-60 day processing period, but it can vary.

What is the minimum credit score needed for an FHA loan?

An FHA loan generally has a lower credit score requirement than a conventional loan. While there isn’t a hard minimum, a score of 500 or above is often needed, though individual lenders may have slightly different requirements. Furthermore, the lender may consider other factors beyond the credit score, such as income stability and debt-to-income ratio.