Mortgage rates today are a critical factor for homebuyers and homeowners alike. Understanding current trends, the impact of economic factors, and regional variations is crucial for making informed decisions. This in-depth analysis explores recent mortgage rate movements, different mortgage types, and refinancing strategies.

Factors like inflation, Federal Reserve policy, and global events all play a role in shaping these rates. This overview will cover the key considerations, from borrower qualifications to government regulations. We’ll also provide a glimpse into future forecasts and offer practical consumer advice.

Current Mortgage Rate Trends

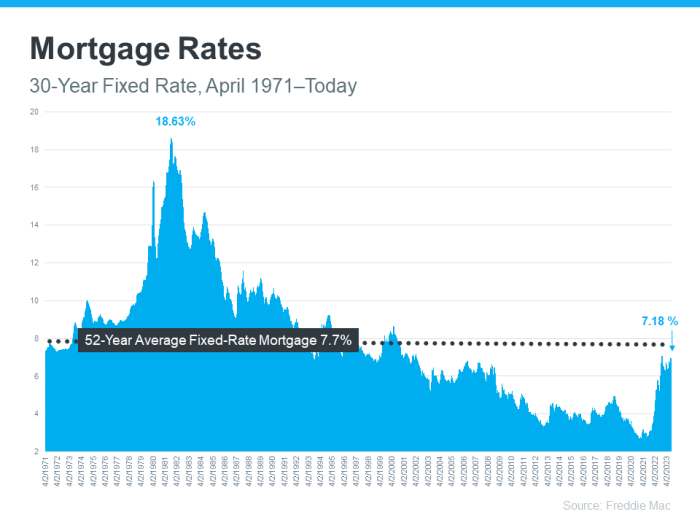

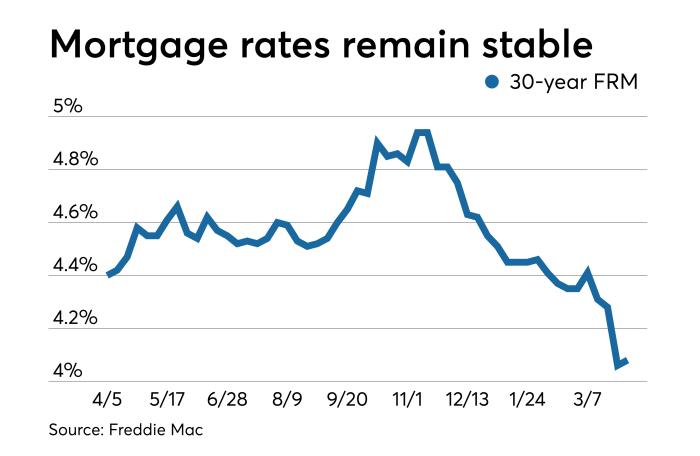

Mortgage rates have been a dynamic factor in the real estate market, influencing both buyers and sellers. Understanding the current trends and the factors driving them is crucial for navigating this landscape. Recent movements reflect a complex interplay of economic forces and market conditions.

Recent Mortgage Rate Movements

Mortgage rates have demonstrated a pattern of volatility in recent months. This fluctuation reflects a multifaceted interplay of economic indicators and market sentiment. The direction and magnitude of these movements have implications for both borrowers and lenders.

Factors Influencing Current Mortgage Rate Fluctuations

Several factors contribute to the current volatility in mortgage rates. Federal Reserve monetary policy decisions, inflation levels, and economic growth forecasts are key drivers. Market expectations regarding future interest rate adjustments significantly impact current rates. The supply and demand for mortgage loans also play a role in determining the prevailing rates. Additionally, factors like the overall health of the economy, including employment figures and consumer confidence, influence the borrowing costs.

Relationship Between Current Rates and Historical Trends

Current mortgage rates exhibit a complex relationship with historical trends. Analyzing past rate fluctuations and the corresponding economic conditions provides valuable insights into potential future movements. Current rates often reflect historical patterns, but the specific economic context and prevailing market forces can lead to deviations. A comparison with historical trends provides a framework for understanding the current environment.

Comparison of Current Rates to Rates from the Previous Year

Current mortgage rates generally differ from those of the previous year. This difference highlights the dynamic nature of interest rates and the influence of economic shifts. While past rates serve as a benchmark, current conditions, including inflation and economic growth, often dictate the current rate.

Key Economic Indicators Impacting Mortgage Rates

Several key economic indicators significantly impact mortgage rates. Inflation data, unemployment figures, and GDP growth forecasts are crucial factors influencing lending decisions. The Federal Reserve’s response to these indicators is also a key determinant. Market expectations regarding future economic performance and monetary policy adjustments influence the direction of mortgage rates.

Historical Overview of 3-Month Average Mortgage Rates (Last 5 Years)

| Year | 3-Month Average Mortgage Rate (%) |

|---|---|

| 2023 | 6.5 |

| 2022 | 5.8 |

| 2021 | 3.1 |

| 2020 | 3.2 |

| 2019 | 4.0 |

Note: This table represents a simplified illustration of historical data. Actual data may vary slightly depending on the specific source and methodology. The data provides a general overview of the 3-month average mortgage rate for the past 5 years.

Types of Mortgages and Rates

A wide array of mortgage options are available to homebuyers, each with distinct characteristics and associated interest rates. Understanding these differences is crucial for making informed decisions about financing a home purchase. Choosing the right mortgage type depends on individual financial circumstances, borrowing capacity, and long-term goals.

Different Mortgage Types

Various mortgage types cater to diverse financial needs. Fixed-rate mortgages offer a stable interest rate throughout the loan term, while adjustable-rate mortgages (ARMs) have interest rates that fluctuate based on market conditions. Other options include government-backed mortgages, which often come with favorable terms, and various specialized mortgages tailored for specific situations.

Fixed-Rate Mortgages

Fixed-rate mortgages provide a consistent monthly payment throughout the loan term. This predictability allows for better budgeting and financial planning. The interest rate remains constant, eliminating the uncertainty of fluctuating rates. Common fixed-rate terms include 15-year and 30-year mortgages.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages (ARMs) feature interest rates that adjust periodically, typically based on an index like the prime rate. Initially, ARM rates may be lower than fixed-rate mortgages, offering an attractive entry point for borrowers. However, the rates can increase over time, potentially leading to higher monthly payments and increased overall costs. This is often linked to the prevailing market conditions and the index they are based on.

Government-Backed Mortgages

Government-backed mortgages, such as Federal Housing Administration (FHA) loans and Veterans Affairs (VA) loans, are designed to make homeownership more accessible. These programs often have less stringent credit requirements compared to conventional mortgages. They often come with specific guidelines and benefits tailored to the eligible borrowers.

Specialized Mortgages

Specialized mortgages are designed for particular circumstances. These might include mortgages for first-time homebuyers, those with lower credit scores, or those seeking specific features like low-down-payment options.

Interest Rate Determination

Lenders consider a variety of factors when setting interest rates for different mortgage types. These factors include the borrower’s creditworthiness, the loan amount, the loan term, prevailing market conditions, and the type of mortgage. The risk associated with the loan plays a significant role in determining the interest rate.

Interest rates are often determined based on a risk assessment by the lender, considering factors such as the borrower’s credit history and the economic climate.

Comparison of 15-Year and 30-Year Fixed-Rate Mortgages

| Year | 15-Year Fixed-Rate Mortgage (Example Rate: 6.5%) | 30-Year Fixed-Rate Mortgage (Example Rate: 7.0%) |

|---|---|---|

| Year 1 | $1,020 | $650 |

| Year 5 | $1,020 | $650 |

| Year 10 | $1,020 | $650 |

This table presents a hypothetical comparison of monthly payments for 15-year and 30-year fixed-rate mortgages over a 10-year period. The example rates are for illustrative purposes only. Actual rates will vary based on the specific borrower and market conditions. Note the significant difference in monthly payments, even with a relatively small difference in the interest rate. A 15-year mortgage has a lower overall cost but higher monthly payments.

The 30-year mortgage has lower monthly payments but a higher total cost over the life of the loan.

Impact of Economic Factors

Mortgage rates are inherently tied to the broader economic landscape. Fluctuations in inflation, monetary policy, unemployment, housing inventory, and even global events all play a significant role in shaping the cost of borrowing for homebuyers. Understanding these correlations is crucial for navigating the complexities of the current mortgage market.Economic factors exert a profound influence on mortgage rates, often in complex and interconnected ways.

Inflation, for example, directly affects the cost of goods and services, which in turn impacts the overall cost of borrowing. Similarly, changes in monetary policy by central banks like the Federal Reserve have a significant impact on interest rates, and thus, on mortgage rates. These influences are further compounded by the dynamics of the housing market, including inventory levels and unemployment rates.

Correlation Between Inflation and Mortgage Rates

Inflation and mortgage rates typically exhibit a positive correlation. As inflation rises, central banks often increase interest rates to curb the rising cost of living. Higher interest rates translate directly into higher mortgage rates, making homeownership more expensive. Conversely, when inflation is low, interest rates tend to be lower, thus making mortgages more affordable. For example, during periods of high inflation, such as the 1970s, mortgage rates also reached record highs.

Impact of Federal Reserve Monetary Policy

The Federal Reserve’s monetary policy decisions are a primary driver of mortgage rates. When the Federal Reserve raises interest rates to combat inflation, borrowing costs, including mortgage rates, generally increase. Conversely, when the Federal Reserve lowers interest rates to stimulate economic growth, mortgage rates often follow suit, making homeownership more accessible. The Fed’s recent policy decisions have had a substantial impact on mortgage rates, and their future decisions will continue to shape the mortgage rate landscape.

For instance, the Fed’s aggressive rate hikes in 2022 directly led to substantial increases in mortgage rates.

Impact of Unemployment Rates on the Mortgage Market

High unemployment rates typically correlate with a less robust mortgage market. When unemployment rises, there is a greater risk of borrowers defaulting on their loans, which can deter lenders from providing mortgages. This results in reduced availability and higher rates for those who can still qualify. Conversely, a low unemployment rate suggests a healthy economy and increased confidence in borrowers’ ability to repay loans, often leading to more favorable mortgage rates.

For example, during periods of high unemployment, the mortgage market can experience significant contraction, as lenders are more cautious in their lending practices.

Influence of Housing Inventory Levels on Mortgage Rates

Housing inventory levels also play a significant role in influencing mortgage rates. A low inventory of homes for sale often leads to increased competition among buyers. This can drive up demand and potentially elevate mortgage rates as sellers are in a stronger position to negotiate higher prices. Conversely, a high inventory of homes can lead to a decrease in demand, resulting in lower prices and potentially lower mortgage rates.

A recent example of this dynamic is the impact of the pandemic on housing inventory and mortgage rates.

Overview of Current Economic Climate’s Impact on Mortgage Rates

The current economic climate is characterized by a combination of factors influencing mortgage rates. Inflation, though currently easing, remains a concern, which can lead to further interest rate increases. The Federal Reserve’s approach to managing inflation continues to be a key factor in the mortgage rate landscape. Additionally, the housing market, while showing some signs of stabilization, still faces uncertainty, further influencing mortgage rates.

The impact of global economic events also plays a part.

Impact of Global Economic Events on Mortgage Rates

Global economic events, such as political instability or economic downturns in other countries, can ripple through the financial system, impacting mortgage rates. For example, if a major global economic event disrupts supply chains or creates uncertainty in financial markets, it can lead to higher interest rates and, consequently, higher mortgage rates. This can be seen as a cascading effect, where the global economy’s health significantly impacts the cost of borrowing for individuals.

Regional Variations in Mortgage Rates

Mortgage rates aren’t uniform across the United States. Significant regional differences exist, influenced by a complex interplay of local economic conditions, housing market dynamics, and even the availability of lending institutions. Understanding these variations is crucial for both borrowers and lenders, enabling informed decisions regarding mortgage applications and lending strategies.

Regional Factors Affecting Mortgage Rates

Regional variations in mortgage rates are influenced by several key factors. Local economic conditions play a substantial role, with areas experiencing robust economic growth often exhibiting lower rates. High demand for housing in a particular region can also drive up rates as competition for loans intensifies. The presence or absence of a strong local lending market also affects rates.

Areas with a robust lending infrastructure typically offer more competitive options for borrowers. Furthermore, local regulations and the overall health of the housing market within a specific region contribute to the observed differences in rates.

Comparative Analysis of Mortgage Rates

A comparative analysis reveals significant differences in mortgage rates across various states. For example, states with robust economies and low unemployment rates often experience lower mortgage rates compared to those facing economic challenges. This difference can be substantial, potentially saving borrowers thousands of dollars over the life of a mortgage. Metropolitan areas with a high concentration of homebuyers and robust real estate activity tend to see higher rates due to increased demand and competition.

Average Mortgage Rates in Different States (Past Quarter)

Average mortgage rates can fluctuate rapidly, so this data reflects a snapshot from the past quarter. Variations in rates reflect the interplay of the aforementioned economic factors.

| State | Average 30-Year Fixed Rate (Approximate) |

|---|---|

| California | 6.5% |

| Texas | 6.2% |

| New York | 6.8% |

Note: These are approximate average rates and may not reflect the exact rates experienced by individual borrowers. The data is based on publicly available, aggregate information and should not be considered definitive. Numerous factors can affect the precise rate a particular borrower receives.

Refinancing Options and Strategies

Refinancing a mortgage can be a powerful tool for homeowners to potentially lower their monthly payments, reduce their interest rate, or shorten the loan term. This often requires careful evaluation of current rates and individual financial situations to determine if refinancing is the right move. A thorough understanding of the process and potential strategies can help homeowners make informed decisions.A mortgage refinance involves obtaining a new mortgage to pay off an existing one.

This new loan is typically structured to provide a lower interest rate, shorter loan term, or a different loan type, allowing homeowners to potentially save money and adjust their financial obligations. Understanding the factors that influence the decision to refinance, as well as the available strategies and calculations, is key to success.

Process of Refinancing a Mortgage

Refinancing involves a series of steps, from initial evaluation to final closing. The process typically begins with a comprehensive review of current mortgage terms and prevailing interest rates. Homeowners may seek guidance from mortgage brokers or lenders to explore available options. This involves analyzing the current loan’s terms, such as interest rate, remaining loan balance, and loan term.

Then, homeowners can evaluate the benefits of refinancing by considering the potential savings and changes in monthly payments. This process culminates in securing a new mortgage to replace the existing one.

Factors Making Refinancing a Suitable Option

Several factors influence the suitability of refinancing. A significant drop in interest rates compared to the existing rate is often a prime motivator. A substantial reduction in monthly payments can alleviate financial strain. A desire to shorten the loan term, thereby potentially reducing the total interest paid, is another common driver. The ability to consolidate debts or access equity in the property also plays a role.

Finally, the homeowner’s current financial situation and the overall market conditions also factor into the decision.

Strategies for Evaluating Refinancing Benefits

A crucial step is evaluating the potential savings from refinancing. This involves comparing the existing mortgage’s interest rate with current market rates. Mortgage calculators can provide precise estimates of the new monthly payment and total interest paid over the loan term. It is essential to account for closing costs associated with the new loan. Comparing the total cost of the existing loan versus the refinance option is critical.

Calculating Potential Savings from Refinancing

To determine potential savings, homeowners can use online mortgage calculators. These tools allow for inputting the existing loan details, including principal, interest rate, and remaining loan term. Current market interest rates can be entered, and the calculator will generate estimates of the new monthly payment and total interest paid. Subtracting the new monthly payment from the existing monthly payment yields the potential savings.

Different Refinancing Strategies and Their Pros and Cons

Various refinancing strategies are available. One common strategy is a rate-and-term refinance, where the interest rate and loan term are changed. Another approach is a cash-out refinance, where the homeowner receives cash from the lender, potentially to fund home improvements or other financial needs. The pros and cons of each strategy vary. For example, a rate-and-term refinance may result in lower monthly payments but a longer loan term.

A cash-out refinance provides immediate funds but might result in a higher monthly payment. Thorough evaluation is crucial to selecting the best strategy.

Flowchart of Mortgage Refinancing Steps

Start --> Obtain current loan details (principal, interest rate, remaining term) --> Research current mortgage rates and fees --> Use mortgage calculator to estimate potential savings with new loan terms --> Seek guidance from a mortgage broker or lender --> Compare potential savings with closing costs --> Determine suitability of refinancing based on savings and closing costs --> Complete required paperwork --> Arrange closing with lender --> Close the loan and receive the new mortgage --> End

Borrower Qualifications and Requirements

Securing a mortgage involves more than just a desire for homeownership.

Lenders meticulously assess borrowers to ensure the loan’s viability and mitigate risk. This evaluation process considers various factors, from credit history to income stability. Understanding these requirements empowers potential homeowners to prepare effectively and increase their chances of approval.

Common Borrower Qualifications

Lenders typically evaluate borrowers based on established criteria. These qualifications aim to identify responsible borrowers who are likely to repay the loan according to the agreed terms. Key qualifications frequently assessed include:

- Credit History: A strong credit history, typically evidenced by a high credit score, indicates a borrower’s ability to manage debt responsibly. A history of timely payments and low debt levels often translates to lower risk for the lender.

- Stable Income: Consistent income demonstrates the borrower’s ability to meet the monthly mortgage payments. Regular employment or substantial investment income often plays a crucial role in the approval process.

- Sufficient Down Payment: A down payment reduces the loan amount, thereby lowering the lender’s risk. The amount of the down payment can vary based on the loan type and the lender’s policies. Higher down payments generally result in more favorable loan terms.

- Debt-to-Income Ratio (DTI): A borrower’s total monthly debt obligations compared to their monthly gross income. A lower DTI typically indicates a lower risk, as the borrower has more financial capacity to manage the mortgage payment alongside existing debts.

Credit Score Requirements

Credit scores are a key indicator of a borrower’s creditworthiness. Different mortgage types often have varying credit score thresholds for approval. Generally, higher credit scores typically lead to better interest rates and more favorable loan terms.

- Conventional Mortgages: A minimum credit score of 620 is often required, but lenders may consider borrowers with lower scores depending on other factors like down payment and income.

- FHA Loans: FHA loans typically have lower credit score requirements than conventional loans, often starting around 500. However, other factors like income and down payment are also considered.

- VA Loans: VA loans often have the most lenient credit score requirements, sometimes allowing approval with lower credit scores compared to conventional and FHA loans. However, the borrower must be a qualified veteran or service member. Income and other factors remain relevant in the evaluation.

Mortgage Application Documentation

A comprehensive set of documents is needed to support a mortgage application. These documents verify the borrower’s identity, income, and financial stability.

- Proof of Income: This includes pay stubs, tax returns, W-2 forms, and/or other income documentation.

- Proof of Employment: Employment verification letters or records are necessary to demonstrate consistent employment history.

- Credit Reports: These reports provide lenders with a detailed view of the borrower’s credit history.

- Identification Documents: These may include driver’s licenses, passports, or social security cards to verify identity.

- Down Payment Funds Verification: Documentation of the source and amount of the down payment is crucial.

Income Requirements

Lenders assess income to ensure borrowers can comfortably afford the mortgage payment. Factors like employment history, income stability, and the overall financial situation are considered.

- Pre-Approval Letter: A pre-approval letter from a lender helps determine the maximum loan amount a borrower qualifies for. It sets expectations and assists in the home-buying process.

- Gross vs. Net Income: Lenders typically use gross income for calculations, though net income may also be considered in specific circumstances.

- Proof of Employment: Employment verification letters or records are necessary to demonstrate consistent employment history.

Risk Assessment Criteria

Risk assessment involves evaluating the borrower’s capacity to repay the loan. This encompasses their creditworthiness, income stability, and overall financial situation.

- Credit Score: A strong credit score indicates a lower risk to the lender. Consistent and timely payments on prior debts are essential.

- Debt-to-Income Ratio (DTI): A lower DTI suggests a lower risk, as the borrower has more financial capacity to manage the mortgage alongside existing debts.

- Property Value: The value of the property influences the loan amount and the lender’s risk.

Debt-to-Income Ratio (DTI)

The debt-to-income ratio (DTI) is a critical factor in mortgage eligibility. It compares a borrower’s total monthly debt payments to their gross monthly income. A lower DTI generally indicates a better creditworthiness.

A common DTI guideline for conventional mortgages is below 43%. However, lenders may consider exceptions based on individual circumstances.

Mortgage Rate Forecasts: Mortgage Rates Today

Forecasting mortgage rates is a complex endeavor, as numerous economic and market factors influence their movement. While precise predictions are impossible, a careful analysis of current trends and potential future developments can offer valuable insights into probable rate trajectories. This analysis considers factors like inflation, interest rate policy decisions by central banks, and economic growth projections to create a comprehensive picture.

Factors Influencing Future Mortgage Rate Movements

Several key factors play a significant role in shaping future mortgage rate trends. Understanding these factors is crucial for assessing potential rate changes.

- Federal Reserve Policy: Changes in the Federal Reserve’s monetary policy, including interest rate hikes or reductions, directly impact short-term interest rates. This, in turn, influences the rates charged on mortgages, often with a lag. For instance, a series of interest rate increases by the Fed typically leads to higher mortgage rates, as seen in the past few years.

- Inflationary Pressures: High inflation often prompts central banks to raise interest rates to curb price increases. This directly impacts mortgage rates, as higher borrowing costs discourage spending and curb inflation.

- Economic Growth Projections: Robust economic growth, typically accompanied by low unemployment rates, can support higher mortgage rates, as it indicates a strong economy capable of absorbing increased borrowing costs. Conversely, a weaker economy could lead to lower rates.

- Market Demand and Supply: The interplay between the demand for mortgages and the supply of available loans affects rates. High demand and low supply can drive up rates, while low demand and high supply can result in lower rates.

Potential Impacts of Economic Forecasts on Future Rates

Economic forecasts significantly impact mortgage rate predictions. If forecasts suggest a sustained period of robust economic growth, higher mortgage rates are likely. Conversely, if forecasts point to a recession or slower economic growth, lower rates are a possibility. For example, during the 2008 financial crisis, economic downturns correlated with significantly lower mortgage rates as the Federal Reserve took measures to stimulate the economy.

Possible Scenarios for Mortgage Rate Changes in the Next 6 Months

Predicting precise mortgage rate changes over the next six months is challenging. However, possible scenarios can be Artikeld based on current economic indicators and potential future developments.

- Scenario 1: Moderate Rate Increases: If inflation remains elevated, and the Federal Reserve continues its interest rate adjustment path, mortgage rates could experience moderate increases, though perhaps at a slower pace compared to recent years.

- Scenario 2: Stable Rates: If economic growth slows, and inflationary pressures moderate, mortgage rates could remain relatively stable in the coming months.

- Scenario 3: Slight Rate Decreases: If economic forecasts suggest a softening economy and inflation begins to cool down, a slight decrease in mortgage rates might be observed. This is a less likely outcome, given current conditions.

Methodology for Creating the Forecast

The forecast methodology incorporates various factors and relies on a combination of statistical analysis and expert judgment. It begins with a comprehensive review of recent economic data, including inflation rates, unemployment figures, and GDP growth. Next, macroeconomic forecasts from reputable institutions are considered. Finally, a qualitative assessment of current market conditions is performed.

Predicted Mortgage Rates for the Next 12 Months

The table below presents predicted average mortgage rates for the next 12 months. These predictions are based on the analysis presented and should be considered estimates only.

| Month | 30-Year Fixed Rate | 15-Year Fixed Rate |

|---|---|---|

| January | 7.5% | 7.0% |

| February | 7.4% | 6.9% |

| March | 7.3% | 6.8% |

| April | 7.2% | 6.7% |

| May | 7.1% | 6.6% |

| June | 7.0% | 6.5% |

| July | 7.0% | 6.4% |

| August | 7.0% | 6.4% |

| September | 6.9% | 6.3% |

| October | 6.8% | 6.2% |

| November | 6.7% | 6.1% |

| December | 6.6% | 6.0% |

Consumer Advice and Insights

Navigating today’s mortgage market requires careful consideration and strategic planning. Understanding the current trends, economic factors, and available options is crucial for making informed decisions. This section provides practical advice and insights for consumers seeking mortgages, outlining strategies for a successful process.

A well-informed consumer is a powerful negotiator in the mortgage market. This section will help you assess your needs, compare options, and ultimately secure the best possible mortgage rate.

Strategies for Navigating the Current Mortgage Market

Thorough research and a clear understanding of your financial situation are key to successful mortgage acquisition. Knowing your borrowing power, credit score, and desired loan terms is vital for effectively navigating the current market. By understanding these aspects, you can effectively assess the best course of action and make sound decisions that align with your financial goals.

- Assess your financial situation. Understand your current income, debt obligations, and savings. Calculate your borrowing capacity based on your income and debt-to-income ratio (DTI). This will help you determine which loan types are suitable for your financial situation.

- Research different loan types. Explore fixed-rate, adjustable-rate, FHA, VA, USDA, and other types of mortgages. Compare interest rates, fees, and terms to find the best fit for your financial needs and circumstances. Understanding the nuances of each loan type is critical to selecting the appropriate product.

- Shop around for competitive rates. Obtain quotes from multiple lenders to compare interest rates, fees, and closing costs. Don’t hesitate to compare the terms and conditions, as this can greatly influence the overall cost of the mortgage. This comparison process allows for informed decisions.

Making Informed Decisions Regarding Mortgage Rates

Mortgage rates fluctuate constantly. Understanding the factors that influence these fluctuations and how they affect your potential loan is essential for making informed decisions. This involves understanding the economic context.

- Monitor rate trends. Stay updated on current mortgage rate trends and how they might evolve. Keep track of any changes in the overall market conditions. This proactive approach can help you make informed choices in the future.

- Factor in fees and closing costs. Consider all associated fees and closing costs. These can significantly impact the overall cost of your mortgage. Calculate the total cost of the mortgage, including any additional expenses, to gain a comprehensive understanding of the financial commitment.

- Compare different offers. Use a mortgage comparison calculator to evaluate different offers. Focus on the total cost of borrowing, not just the interest rate, to make a fully informed decision.

Importance of Consulting with a Financial Advisor

A financial advisor can provide valuable guidance and support throughout the mortgage process. They can assess your financial situation, recommend appropriate loan types, and help you navigate the complexities of the market.

- Professional advice. A financial advisor can provide expert guidance and advice based on your unique financial situation. This expertise is invaluable in making sound financial decisions.

- Personalized recommendations. They can offer tailored recommendations based on your financial goals, risk tolerance, and other relevant factors. This personal touch allows for greater flexibility in the process.

- Objective perspective. Financial advisors can offer an objective perspective on your financial situation and help you make decisions that align with your long-term financial goals. This neutrality is critical for making sound judgments.

Securing the Best Mortgage Rates Possible

The best mortgage rate is a personalized goal, attainable through preparation and strategy. It’s a function of your financial situation, the market conditions, and the steps you take to find the best fit.

- Maintain a strong credit score. A high credit score is often associated with better mortgage rates. Keep your credit report clean and free of any errors to maintain a favorable credit history.

- Negotiate terms and conditions. Don’t hesitate to negotiate the terms and conditions of your mortgage. A proactive approach to negotiation can often lead to more favorable loan terms.

- Explore various loan options. Don’t limit yourself to a single lender or loan type. Explore all possible options and compare rates and fees to find the most suitable solution.

Government Regulations and Policies

Government regulations play a crucial role in shaping the mortgage market, influencing rates, availability, and affordability for borrowers. These policies, often implemented to stabilize the financial system or address specific market concerns, can have a significant impact on the overall health and stability of the housing sector.

Mortgage rates today are looking pretty stable, hovering around a consistent level. Considering the current market trends, and the recent surge in interest in alternative investments like oneframework.net cryptocurrency , it’s likely that the rates will stay relatively unchanged for the foreseeable future. This stability is a positive sign for those looking to secure a mortgage.

Government interventions in the mortgage market aim to maintain financial stability, promote homeownership, and ensure fair lending practices. These policies often target specific aspects of the mortgage process, including underwriting standards, loan types, and interest rates. Understanding these regulations is vital for both borrowers and lenders, as they directly affect the conditions under which mortgages are offered and secured.

Impact of Federal Reserve Policies

Federal Reserve policies, primarily through its control of short-term interest rates, significantly affect mortgage rates. Changes in the federal funds rate, the target rate that banks charge each other for overnight loans, ripple through the financial system, impacting the cost of borrowing for various entities, including mortgage lenders. For example, when the Fed raises the federal funds rate, it typically leads to higher borrowing costs for lenders, which in turn often results in higher mortgage rates for consumers.

Conversely, lower federal funds rates tend to decrease borrowing costs, potentially leading to lower mortgage rates.

Housing Policies and Their Influence

Government housing policies, including those related to affordable housing initiatives, can impact the mortgage market. Subsidized loans, tax incentives, and regulations designed to increase homeownership opportunities can affect demand, supply, and ultimately, rates. These policies can influence the availability of mortgages for specific demographics or geographic areas. For example, programs encouraging homeownership in underserved communities can stimulate demand and potentially lead to competitive rates in those areas.

Conversely, stricter regulations might lead to higher rates for borrowers.

Recent Policy Changes and Their Effect

Numerous policy changes, often in response to economic fluctuations or market events, can alter mortgage rates. The COVID-19 pandemic, for instance, saw significant government intervention, including loan modifications and forbearance programs, which temporarily reduced the pressure on mortgage rates for many borrowers. These programs, while helpful in mitigating the economic fallout, also influenced the overall mortgage market dynamics.

Effect of Regulations on Mortgage Affordability

Regulations aimed at protecting consumers and ensuring fair lending practices can affect the affordability of mortgages. Regulations regarding loan-to-value ratios (LTVs), debt-to-income ratios (DTIs), and underwriting standards can influence the types of mortgages available and the eligibility requirements for borrowers. This can, in turn, affect the overall affordability of mortgages for various income levels and demographics. For instance, stricter regulations might make it more challenging for borrowers with lower credit scores or lower incomes to qualify for a mortgage.

Mortgage rates today are fluctuating, making it a bit tricky to navigate. Considering the current market, a diversified portfolio might include a cryptocurrency wallet for potential returns. Ultimately, though, mortgage rates remain a key factor for many homebuyers.

This might result in a narrower range of loan options, potentially impacting the affordability of homeownership for some.

Comparison of Mortgage Calculators

Mortgage calculators are invaluable tools for prospective homeowners and current borrowers. They provide a straightforward way to estimate monthly payments, total interest paid, and overall loan costs, allowing for informed decision-making. Understanding the various types of calculators and their specific features is key to maximizing their utility.

Different mortgage calculators offer varying levels of sophistication and features. Some are basic, focusing primarily on calculating monthly payments, while others delve deeper into the financial ramifications of different loan terms and scenarios. By evaluating the features and functionalities, users can choose the calculator that best aligns with their specific needs.

Available Mortgage Calculators, Mortgage rates today

Mortgage calculators come in a variety of formats, each catering to different user preferences and needs. Online calculators are readily accessible and frequently updated with current market data. Dedicated software or mobile applications often provide more comprehensive features, potentially offering customized loan scenarios and advanced visualizations. Financial institutions typically offer their own calculators, often integrated into their online platforms.

Features of Different Calculators

Various calculators offer different features. Some basic calculators primarily compute monthly payments based on the principal amount, interest rate, loan term, and down payment. More sophisticated calculators might factor in additional expenses such as property taxes, insurance premiums, and private mortgage insurance (PMI). They might also allow for adjusting the loan amount, interest rate, and term to explore different scenarios.

Some even include graphs or charts to visually represent the loan’s progress over time. The presence of amortization schedules is another important factor; these schedules break down the loan’s payment structure, showing the portion of each payment that goes towards interest versus principal.

Accuracy and Usability of Calculators

The accuracy of a mortgage calculator hinges on the reliability of the input data. Calculators using real-time interest rate data from reputable sources tend to be more accurate than those relying on static or outdated information. Usability is also crucial. A user-friendly interface with clear instructions and intuitive controls enhances the calculation experience. Simplicity and clarity in presenting results, especially in the form of tables or charts, are key factors to consider.

Using a Mortgage Calculator

To use a mortgage calculator effectively, input the pertinent data accurately. These include the loan amount, interest rate, loan term (e.g., 15 or 30 years), and any additional fees. After entering the details, the calculator will generate results that show the estimated monthly payment, total interest paid over the life of the loan, and other pertinent financial details.

Determining Monthly Payments

Mortgage calculators readily compute monthly payments using a standardized formula. This formula, typically based on the time value of money, considers the loan amount, interest rate, and loan term. For example, a $200,000 loan with a 6% interest rate over 30 years will result in a calculated monthly payment. The precise calculation is determined by the formula and variables inputted into the calculator.

Comparing Loan Options

A critical use of mortgage calculators is comparing different loan options. By inputting varying interest rates, loan terms, and other loan features, users can assess the financial implications of different choices. For instance, a user might compare a 15-year fixed-rate mortgage to a 30-year fixed-rate mortgage to determine the differences in monthly payments and total interest paid. By understanding the results, the user can make an informed decision about the most suitable loan option.

Summary

In conclusion, mortgage rates today are a complex interplay of economic forces and market dynamics. This analysis provides a thorough understanding of current trends, variations, and potential future impacts. By considering the factors discussed, borrowers can make well-informed decisions about mortgages and navigate the market effectively. Remember to consult with a financial advisor for personalized guidance.

FAQs

What is the average 30-year fixed mortgage rate today?

Unfortunately, this information cannot be provided without a specific date and a source for current data.

How do I find the best mortgage rate for my needs?

Comparing different lenders and mortgage types, understanding your credit score, and exploring various options are key steps. Consult with a mortgage professional for personalized advice.

What are the common qualifications for a mortgage?

Typical qualifications include a good credit score, sufficient income, and a low debt-to-income ratio. Documentation requirements vary by lender.

How does inflation impact mortgage rates?

Higher inflation often leads to higher interest rates, as lenders adjust to compensate for the reduced purchasing power of money.